Gold & The Upcoming Recession

We are now seeing the initial stages of a currency, credit, and banking crisis develop.

Driving it are an inflation of prices, contraction of bank credit and a pathological fear of recession.

One can imagine that the major central banks almost wish a mild recession upon us so that they can keep interest rates suppressed and bond yields low.

The key to understanding the course of events is that the cycle of bank credit is turning down, and this time the factors driving contraction are greater than anything we have experienced since the 1930s, and possibly in all modern monetary history.

This article joins the dots between inflation and recession and puts the relationship between money (that is only gold), currencies, credit, and commodity prices into their proper perspective.

The bank credit downturn…

It is increasingly obvious that the economic cost of sanctioning Russia is immense, and there’s now growing evidence of all major economies facing a downturn in economic activity. And we don’t have to rely on GDP forecasts to know why. Intuitively, if food and energy shortages impact us all, higher prices for these items alone will affect our spending on less important items and services.

That’s reasonable enough for sensible citizens. But financial analysts insist on quantifying it with their models. Their principal measure is the total value of all recorded transactions, comprised of GDP. They proceed seemingly unaware of the difference between the value of economic activity to the advancement of the human condition, which can’t be measured, and a meaningless total comprised of only currency and credit, which can. Consequently, all they end up recording is changes in the quantity of currency and credit deployed in the economy.

Of course, there is a broad point that if the quantity of currency and credit contracts, GDP falls. And if it is severe, economic activity tends to fall as well. But to equate the two to the point that a variation of less than a per cent or so from modelled forecasts means anything is nonsense. A proper assessment of the economic condition gets lost.

Instead, an awareness of the role of bank credit is called for. Banks create credit, which feeds into the GDP total when they are optimistic about the outlook for lending. And when they deem the outlook to be deteriorating, they withdraw credit which reduces the GDP total. It leads to a repetitive cycle of boom and bust. We are now entering a period where, at the margin, banks are trying to reduce their exposure to credit going sour. Therefore, GDP will contract And we can assess where it will contract. It really is that simple.

The best thing to do is to stand back and let the excesses of lending and the support for malinvestments wash themselves out of the system. The last time this was done was the brief but very sharp recession of 1920—1921 in the US. The government of the day understood it was not its business to intervene, and anyway, it was not capable of improving thngs.

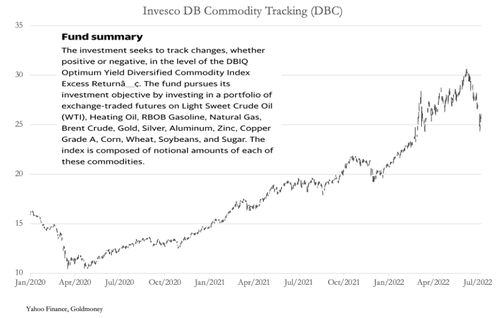

But increasingly since, monetary policy has become run by central banks which steer their economies through rear view mirrors, reacting to information rather than anticipating. But even if they could anticipate economic trends they lack the commercial nous to manage it. Instead, their stock reaction to declining GDP will be to “stimulate”. Not only do they have a mandate to maintain full employment, but they have a Keynesian belief that a decline in GDP is entirely due to falling demand. Falling demand, they say, leads to lower prices, so the inflation figures in the CPI will fall. Producer prices will fall. All commodity prices will fall. The chart below feeds this line of hopeful thinking.

This basket of commodities has fallen in value by 17% in a month. Panic over. Even wheat and soya prices have fallen. Dr Copper is down. Grasping at these straws, central banks are undoubtedly relieved that inflation might be turning transient after all.

Or so they think. There is no doubt that we are experiencing enormous price volatility. If it was entirely due to consumers deciding not to spend because prices are too high for them, that is one thing. But if it is because banks are withdrawing credit, the consequences are materially different.

A central bank’s concern to maintain consumer spending might discourage banks from contracting credit for consumers, at least initially. Furthermore, their risk models show that while individually consumers using credit are often high risk the magic of securitisation turns these risks collectively into low risk. It becomes a numbers game. So, credit card and other consumer faced lending divisions with very high credit margins are not the first to be targeted. And anyway, that would put the bank’s executives at odds with the central bank.

Instead, in the initial stages of a credit downturn, banks withdraw credit principally from business borrowers who use overdraft facilities. A business that frequently resorts to overdraft facilities is high risk in any bank’s assessment. Weaker businesses are first to succumb to the credit downturn for this reason. Other early victims of credit contraction are financial speculators because their collateral is easily realised. We have seen the decline of US stock indices so far being accompanied by a $200bn reduction in margin lending. There’s still much more to go.

As the economist Irving Fisher pointed out in the 1930s, calling in loans to reduce bank credit can become a self-feeding destruction of value. The bit he failed to understand is that in a serious downturn it can’t be helped, because it is the other side of earlier credit expansion, and it is the unwinding of unsound lending. Both an understanding of what drives periodic contractions of bank credit and the empirical evidence that it has repeated in one form or another approximately every decade since records began, inform us that it should not be stopped but allowed to proceed. Compare the brief 1920—1921 slump in the US with the prolonged 1930s slump, the latter managed by first Presidents Herbert Hoover and then Franklin Roosevelt.

We should also know from understanding that bank credit is a cycle, that the height of the recent expansionary phase measured by the ratio of total bank balance sheet assets to their shareholders’ capital indicates the likely severity of the subsequent credit contraction. It reflects deposit liabilities to a bank’s customers relative to its shareholders assets. Traditionally, asset to equity ratios of more than eight to ten times were deemed risky. Some major banks, particularly in the EU and Japan, are now at over twenty times. While the US banks are less geared, the systemic risks to them from other national banking systems in this financially interconnected world are the highest they have ever been.

For the immediate future we can discern two things. First is that production of goods and services is likely to be more limited than consumption due to an absence of bank credit, knocking on the head the Keynesian misconception that it is a problem of insufficient demand. That is just an initial phase. And following it, the contraction of bank credit can be expected to become more severe, as banks draw their horns in to protect their shareholders from an Irving Fisher style slump. In this subsequent second phase both producers and consumers will face enormous financial difficulties.

Without aggressive intervention by central banks, the correction from excessive over-lending taking bank balance sheets beyond dangerous levels of leverage will simply fuel a GDP slump. Central banks will intervene, not just to deliver on the full employment mandate, but to finance government budget deficits which will soar under these developing circumstances.

Prices in a slump

The last real slump, when the forces driving bank credit contraction were arguably less severe, was in the 1930s following the Wall Street crash. At that time, the dollar and sterling, together the world’s major international currencies, were both on gold standards. Prices of commodities, raw materials and agricultural products collapsed, effectively measured in gold through these two currencies. The political strains led to Britain abandoning its bullion standard in 1932, and the US gold coin standard was suspended for US citizens in 1933, followed by a 40% dollar-devaluation in January 1934.

The effect of the collapse of bank credit was to make circulating media in dollars and sterling scarce, thereby raising their purchasing power. To this extent, gold’s purchasing power also rose, because it was tied to the currencies. While gold gave credibility to the dollar and sterling, it was the contraction of bank credit that drove the slump in prices, while gold got the blame.

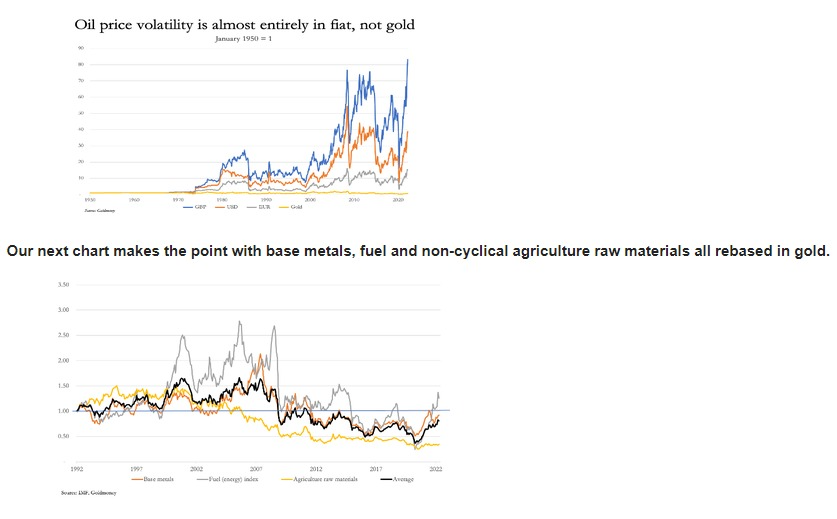

We know that priced in gold, over time commodity, raw materials, and agricultural product prices are remarkably stable. Disruption in the price relationship does not come from gold. The following chart of the WTI oil price rebased to 1950 illustrates prices in sterling, dollars, and euros where there are huge variations in prices. Contrast that with gold (the yellow line), where the price today is down about 30% from 1950 with minimal volatility along the way.

Since 1992, which is the earliest common date we have for these series, an unweighted average gold value for them has fallen a net 19% (the black line). Fuel has been the most volatile at up to 2.5 times the 1992 price, but from the previous chart we can see that it was up a net 12 times in US dollars in 2007/08 from 1992. Priced in gold, the relatively little volatility we see in these commodity groups is as close as we can get to free market values in sound money. And even then, we know that gold prices are manipulated in the markets. We can also assume that the origin of this volatility does not come from gold, but from the violent price changes in fiat currencies, their interest rates, and their distortions with respect to demand for commodities.

These findings overturn conventional opinions on price formation. The evidence is that it is not true that fiat currencies are purely objective in their relationship with commodity prices. Forecasters of commodity prices incorrectly assume there is no change from the currency side. But clearly, the fluctuations overwhelmingly emanate from the currencies themselves.

This brings us to the likely effect of an economic slump on prices. Initially in our analysis, we will assume there is little change in the public’s desire to hold fiat currencies relative to the range of commodities and consumer goods. That being the case, we can see that it will be variations in the quantity of currency and credit in circulation driving prices. A contraction in this quantity will tend to lower prices. And Keynesian economists might conclude that precious metals being commodities will also fall in price against fiat currencies, given that fiat currencies are no longer tied to gold.

The flaw in this argument is that there are indeed other factors involved, and the consequences for the quantity of currency and credit in a slump must be taken into account. Irrespective of changes in monetary policy, in socialised economies government budget deficits soar and will need financing by expansion of the currency if bank credit is not forthcoming. In other words, despite the tendency for banks to contract bank credit to the private sector and even if central banks do not amend monetary policies, it will be more than offset by an expansion of currency passed into the economy through the government’s books.

Furthermore, under these circumstances monetary policy will change as well. Following the initial withdrawal of overdraft credit from businesses and bank loans for financial speculation, there is likely to be a softening of consumer demand as lending standards tighten and financial insecurity for consumers escalates. Central banks will notice the tendency for the withdrawal of bank credit to lead to a slump in consumer demand. They will almost certainly reduce interest rates and reintroduce quantitative easing to replace contracting bank credit to stimulate flagging economic activity. They have eased and stimulated in every bank credit cycle at this point since the 1930s, and there’s no reason to think they will do otherwise today.

An increase in currency and credit, not emanating from the commercial banks but from the central bank, with increasing budget deficits will continue to debase the currency in gold terms. The currency will also be debased against commodities. But with some volatility imparted from the currency side, we can see that the general relationship between commodities and gold can be expected to remain intact.

A systemic failure is on the cards

All this assumes that within the context of the bank credit cycle there is not a significant systemic failure. Given that the forces behind credit contraction today are greater than any time since the 1930s, and possibly for all modern monetary history, that is a vain hope. Last week I pointed out the looming catastrophe for the euro system and the euro. A similar tale can be told about the Japanese yen. And sterling is just a poor man’s version of the dollar without its hegemony status.

In the event of a systemic crisis, the role of central banks will be to underwrite their entire commercial banking system. The consequences of letting Lehman go bankrupt on the last cycle of bank credit contraction did not serve as a warning to profligate bankers. Instead, it had us all staring into a systemic abyss, and that mistake will not be repeated. In a systemic crisis today, it will take unprecedented currency and credit creation by the central banks to save the financial world. And it’s that debasement that will end up collapsing fiat currencies.

Meanwhile, we can expect central banks to milk the transitory inflation story for all its worth. Forget the CPI rising at 8%+ they will say. It will soon return to the 2% target as recession bites. But that’s another excuse to ease policy. It might buy just a little more time before the crisis hits. But don’t bank on it.

Manipulation becomes official

Earlier this month, three JPMorgan Chase traders faced a federal trial in Chicago, accused of masterminding a massive eight-year scheme to manipulate international markets for precious metals by spoofing, including gold and silver. JPMorgan had already been fined $920m in 2020.

Coincidently, Peter Hambro who was a gold trader in London in the early days of the derivatives market described how the bullion banks created unallocated gold accounts. One of Hambros’ more interesting comments was about the role of the authorities:

Read more at: https://www.zerohedge.com/markets/gold-upcoming-recession