Participating in Lavita’s AI training jobs on the Theta Edge Network is an exciting opportunity to contribute to healthcare AI efforts. Lavita jobs will begin with a small dataset for testing purposes that would take less time than the average AI training tasks. This will gradually increase as the datasets become larger.

The minimum hardware requirements are:

- Internet speed: 5Mbps+ up and down

- CPU: 4 cores or more

- Memory: 16GBytes or more

- Free hard drive space: 64GB or more, best with 256GB+ available disk space, which is needed for training large deep learning models.

- GPU (optional): Nvidia GPUs with CUDA enabled. CUDA-enabled GPU can greatly accelerate AI tasks.

Here’s a step-by-step guide on how to get involved:

Step 1 : Set Up Your Theta Edge Node

If you don’t already have a Theta Edge Node running, start by downloading and installing the apps for Windows or macOS. If you want to run the command line version (e.g. on Linux), please refer to this guide which provides instructions to run the Theta Edge Node with docker.

Once you launch the app, you’ll see the Edge node dashboard as follows:

Go to “Settings” and make sure the “Lavita” setting is enabled.

Step 2 : Wait until the Theta edge node connects to your wallet

Once you launch the app, it will create a wallet automatically for new users and existing users will be connected to their existing wallets, as shown in the top-left of the dashboard.

Step 3 : Edge nodes will be assigned with AI training jobs automatically

Your Theta edge node will automatically download datasets that are required for the AI task. These datasets contain medical questions and answers data for training purposes.

Your Theta edge node will also automatically run the AI training code on the dataset provided using your PC’s computational resources. Fine-tuning involves training a pre-trained AI model using a medical dataset prepared by the Lavita platform to further customize for specific medical AI tasks.

Once the fine-tuning process is completed, it will automatically upload the trained model files to the cloud. Lavita platform will download the model files based on your unique Edge Node ID and compute its own hash to verify that the uploaded files are authentic and have not been modified or tampered with.

Once validated, users will be rewarded with LAVITA tokens. The Lavita platform will evaluate the performance of your fine-tuned model against its own test dataset, such as achieving better performance than the baseline model.

Step 4 : Send vLAVITA (Voucher LAVITA) to Theta Wallet in Main Chain

After completing AI training jobs you will receive LAVITA tokens, stored as vLAVITA (voucher-LAVITA). These vLAVITA can be easily transferred to the Theta main chain for use including swapping to other tokens or sent to exchanges.

- Navigate to the Theta Wallet (“OPEN NODE WALLET” button) and select the Lavita subchain from the Mainnet list at the top of the application; you will find vLAVITA added here.

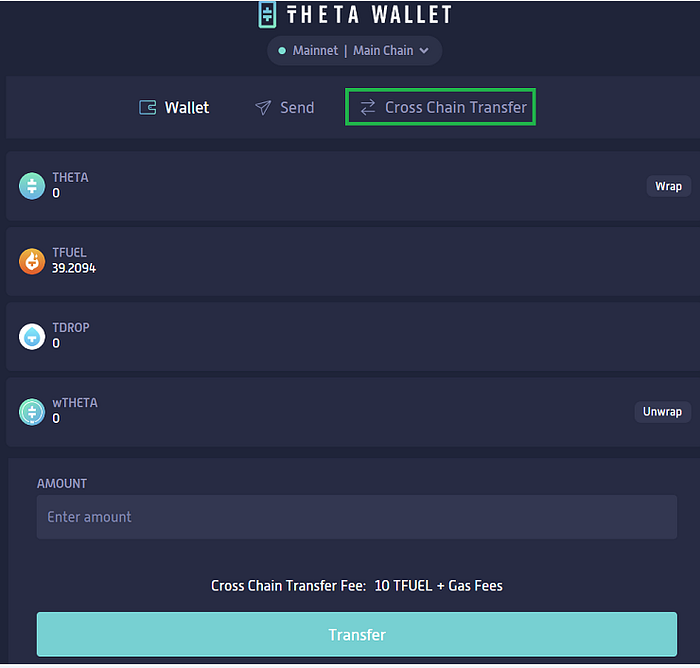

There are TWO ways to transfer vLAVITA to the Theta main chain for LAVITA

1. Sending vLAVITA to any wallet you desire to transfer vLAVITA, and click “Cross-Chain Transfer”

- Click “Send”, then enter address, choose vLAVITA and the desired amount you want to send to your wallet

- Go to your wallet that you received your vLAVITA, click on “Cross Chain Transfer” then choose vLAVITA from ASSET and enter the desired amount you want to send to the Main Chain to get LAVITA. Once the transfer is complete, the amount will be reflected in your LAVITA balance on Theta wallet’s Main Chain display, under the same wallet address.

2. Sending vLAVITA to your Theta node wallet’s Main chain

- Click on “Metachain” then choose vLAVITA and the desired amount you want to send to the Theta Mainnet. Once the transfer is complete, the amount will be reflected in your LAVITA balance on Theta node wallet’s Main Chain display, under the same wallet address. (Make sure to have enough TFUEL transferred into your wallet for the Cross Chain Transfer Fee + Gas Fees)

Continue running Theta edge node for Lavita AI tasks

Keep running the Theta edge node to share your computation resources and watch for announcements. The field of AI is constantly evolving, and there will be new tasks, datasets, and new opportunities in the medical field.

By following these steps, you will actively contribute to Lavita’s collaborative AI ecosystem and help drive advancements in medical AI using NLP. Your efforts will contribute to the development of sophisticated medical AI models with the potential to revolutionize healthcare delivery and research.